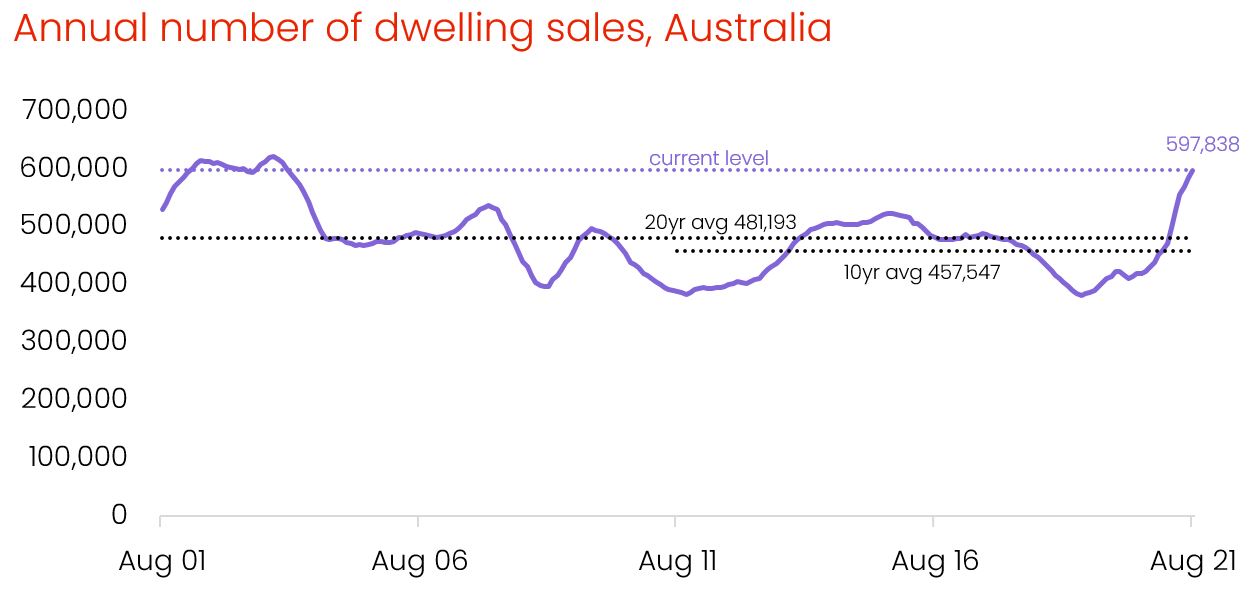

Housing Turnover Reaches The Highest Level In Nearly 12 Years

Housing turnover in Australia is at a new high, and purchase volumes lately have been the highest in years. The number of homes sold last year in Australia was 31% more than the decade average and 24% higher than the 20-year average.

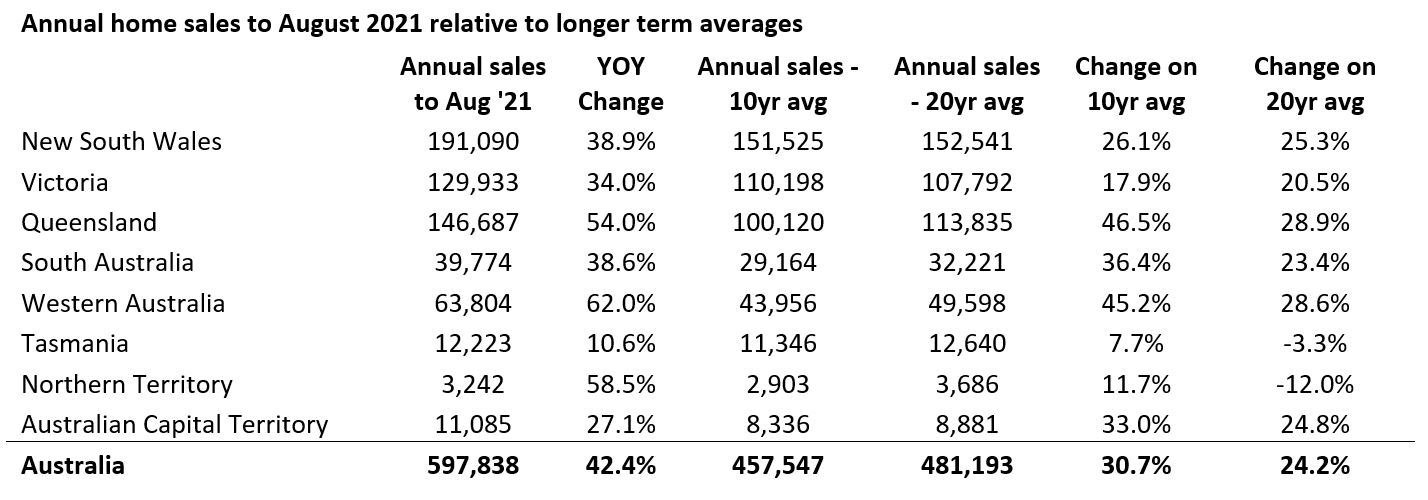

Annual home sales are much higher across the states than they were a year ago, with every state and territory except Tasmania, reporting a year-on-year increase of more than 10%. The lesser increase in sales in Tasmania, where advertised supply was roughly 35% below average at the end of August, is likely due to a lack of supply rather than a demand constraint.

The most significant year-on-year increases in yearly home sales may be found in Western Australia and the Northern Territory, where the market is catching up. Year-on-year home sales have increased by 62 percent and 59 percent in California and Queensland, respectively, with a 54 percent increase in Queensland.

Obtain Bridging Finance

If you buy first and struggle to sell your home, you will most probably need to take out a bridging loan. Typically, interest-only, this is a loan you will have on top of your existing home mortgage loan so that you can service two mortgages simultaneously. Bridging finance can sometimes be at a much higher interest rate, so you should not go into it without seeking financial advice.

Source: Corelogic

While such a large increase in housing demand may appear surprising at a time when international migration has slowed, the big increase in home sales can be explained by a boost in local demand from previously low levels.

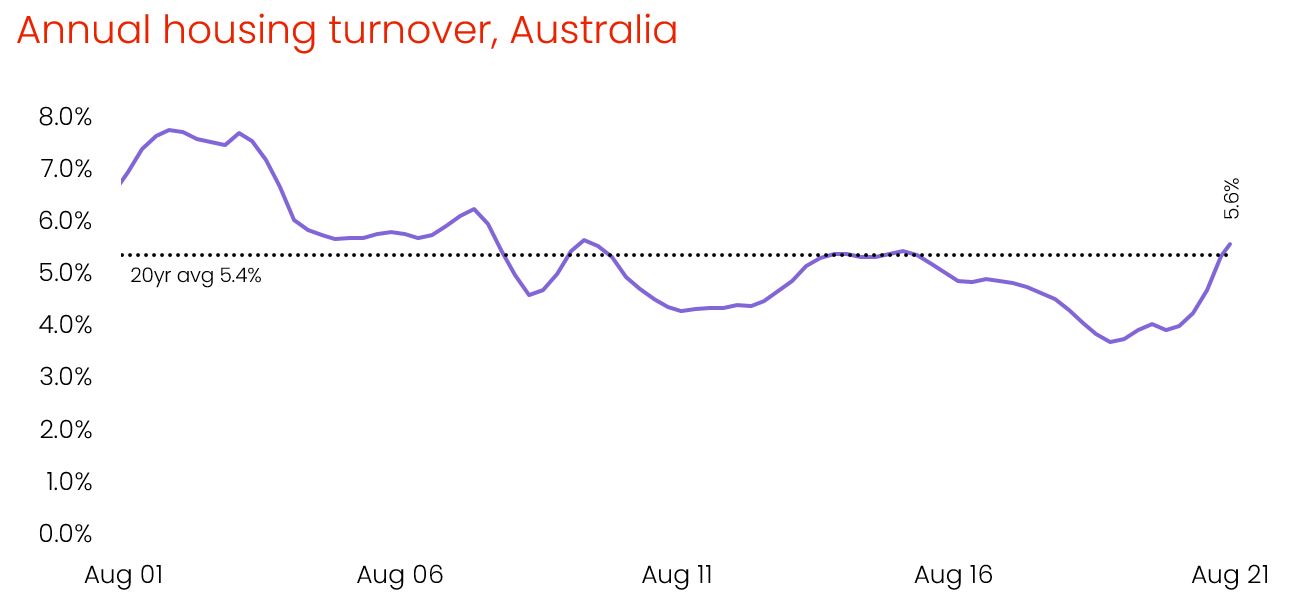

As lending conditions tightened, housing affordability grew more difficult, and transaction fees such as stamp duty became increasingly expensive as prices increased, housing turnover (annual house sales as a percentage of total residences) began to decline in late 2015. In June 2019, national turnover hit a new low, with barely 3.7 percent of Australian houses changing hands for the year. Credit regulations have loosened since then, and mortgage rates have fallen to historic lows, encouraging more Australians to enter the home market. Furthermore, since March 2020, a greater rate of household savings has bolstered consumer deposit levels and mortgage serviceability, while government incentives including stamp duty discounts and deposit guarantees have also encouraged demand.

Housing turnover had surged to 5.6 percent at the end of August 2021, the highest percentage since December 2009.

Source: Corelogic

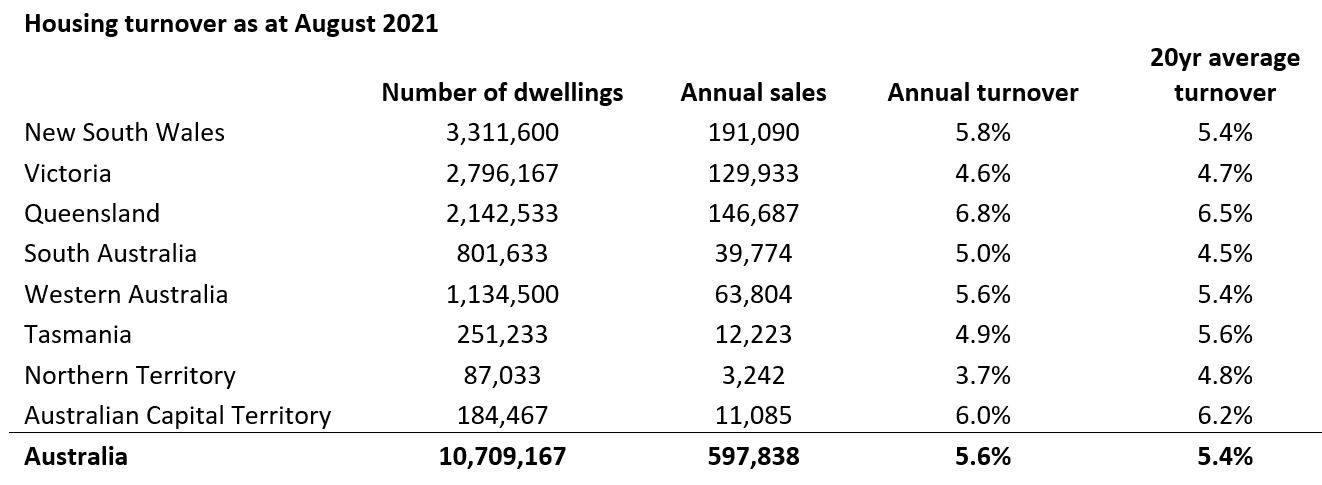

Queensland had the largest turnover of all the states, with 6.8% of properties transacting in the year to August, the Sunshine State’s highest level since the 12-months ended June 2008. A spike in interstate migration, as well as comparatively low home prices compared to New South Wales and Victoria, are supporting the higher rate of turnover.

With 6.0 percent of residences selling in the last year, the ACT has the second highest rate of housing turnover. When house prices are compared to earnings, Canberra’s housing market, like Queensland’s, is relatively inexpensive. A substantial lift in investment activity also helps to explain the higher rate of turnover, with the value of investor lending rising from 17.1% of all lending in January 2020 to almost 31% in July 2021.

The Northern Territory had the lowest turnover, with only 3.7 percent of homes changing in the last year, up from a prior low of only 2.4 percent in June last year. Despite an almost 60 percent increase in home sales over the last year, yearly sales in the NT were still 12 percent below the 20-year average, demonstrating how strong demand has been in previous growth cycles.

The Northern Territory had the lowest turnover, with only 3.7 percent of homes changing in the last year, up from a prior low of only 2.4 percent in June last year. Despite an almost 60 percent increase in home sales over the last year, yearly sales in the NT were still 12 percent below the 20-year average, demonstrating how strong demand has been in previous growth cycles.

Victoria has the second lowest rate of housing turnover in the country, with only 4.6 percent of residences changing hands in the last year. Multiple lockdowns, as well as decreasing housing affordability, have contributed to the lower turnover reading. In addition, a huge number of newly constructed homes have increased the state’s overall housing supply. Victoria’s population has grown by 280,900 people in the last five years, the most of any state or territory.

Housing turnover had surged to 5.6 percent at the end of August 2021, the highest percentage since December 2009.

Source: Corelogic

Given that the yearly number of sales has yet to peak, housing turnover is likely to rise a little more from here. However, we believe that in the medium run, turnover will peak in early 2022. Although reading through the added interruption of lockdowns makes the patterns difficult to discern, there is already indication that the monthly number of home sales is starting to drop.

- Despite the fact that activity may pick up after the lockdown, home sales are anticipated to fall in the medium term due to a number of factors:

- In most capital cities and regional housing markets, the ratio of housing prices to household earnings is reaching new highs. As affordability continues to deteriorate, more purchasers will be unable to participate in the home market.

- A renewed focus on lending standards may exacerbate affordability issues. With policymakers and lenders focusing more on lending quality, it’s likely that borrowers with low deposits or high loan/debt levels compared to their salaries will have a harder time getting a loan.

- An increase in total inventory levels. Even if the number of home sales remains stable, a broad-based boom in residential development activity in Australia could dampen the turnover rate.

- Low to no international migration will gradually reduce home demand. The impact of halted overseas migration rates had a more direct and immediate impact on rental demand, particularly in Melbourne and Sydney’s inner-city high-rise zones (although rents in these inner-city precincts are now rising). However, the demand from permanent migrants, who prefer to rent first and then buy, is unlikely to be replenished for a long time.

The fact that mortgage rates are expected to remain at record lows for an extended period of time offsets these obstacles, and economic conditions should improve as lockdowns relax and labour markets strengthen.

Moving away from property transaction disincentives like stamp duty in the long run would assist foster increased turnover. Transactional fees, along with raising a deposit, were found to be the most significant impediments to house affordability in previous CoreLogic study. It’s heartening to see state governments in the ACTACT, SA, and NSW phasing out stamp duty, albeit with differing tactics and timelines, which should help to reduce barriers to property owners and prospective buyers transacting in the housing market.